< GO BACK

Nothing Else Comes Even Close: The most asymmetric investment class only a few know about

March 17, 2026

/

AIF

The topics I usually write about revolve around the future of banking and the evolution of its business model. In very simplified terms, banks channel money entrusted to them by depositors and create an ecosystem of interconnected cash flows that fuels the economy and supports our daily lives. Yet, when it comes to pure money and asset management, banks are not the only — nor necessarily the best — game in town. Today, I want to step outside the typical banking balance sheet and point to a business model that sits at the very heart of professional asset management. A model that is quietly becoming one of the most attractive — and hardest to access — asset classes in the world.

The one that Forbes 2022 article[1] described as: “Opportunities of these types are rare—even within the institutional space. Access for retail investors will likely always be extremely rare—at best—but can be invaluable as a financial vehicle: affording performance that is not only uncorrelated but generates unmatched absolute risk-adjusted performance. Nothing else comes even close”.

Welcome to the world of General Partners (“GPs”), the firms that manage capital on behalf of professional investors. The capital which is pooled together in the format of an investment fund, usually structured as the entity called limited partnership (“LP”). These firms design investment strategies, raise capital, and deploy that capital into the real economy — into companies, real estate, renewable energy assets, private debt, venture capital, and more. And when a GP becomes consistently good at allocating capital, delivering returns and enjoying repeated trust of those who entrusted it with their money, the GP itself becomes the investment opportunity.

I’m not talking about funds nor the assets inside funds.

But the business that manages the funds.

Opportunity so unique in terms of return / risk characteristics that it deserves the title of this article.

The Core Idea

Everyone who deals with asset management and investments (managing money for 3rd party clients), and everyone who invests their own savings for the better future knows the basic theory: diversification is the only free lunch in finance. Don’t put all the eggs in one basket, no matter how nice the basket looks like, right? Easier said than done. True diversification is difficult unless you have enough capital to spread across multiple asset classes, geographies, and strategies.

Ray Dalio, the founder of Bridgewater Associates, refers to diversification as the “Holy Grail of Investing.” Dalio emphasizes that the key to successful investing lies in constructing a well-diversified portfolio that balances risk and reward across a wide range of uncorrelated asset classes. The idea is rooted in the concept that by holding a diverse array of uncorrelated assets, an investor can significantly reduce overall portfolio risk while maintaining or enhancing expected returns. This strategy works because the likelihood of all asset classes performing simultaneously poorly is low. When one asset class is underperforming, others are likely to be doing better, thereby stabilizing the portfolio’s overall performance.

And while the answer to a question of whether “do you want to bet on a horse or own a piece of the entire racetrack” has always been obvious, there were and still are limited options available for the racetrack purchase because even if you buy an index or ETF fund, you still bet on a single, albeit individually / internally diversified asset class.

The Market Tailwind (and why it’s irreversible)

I have written about the great transition of sources which are funding the economy, because it affects banks. And I observe this trend happening everywhere in the developed world, even at the fragmented markets I operate across.

To re-iterate: In search of higher returns, sophisticated client funds have been growing and migrating out of the banks’ balance sheets - away from corporate and retail deposits, bank bonds and other liabilities - and into vehicles such as sovereign funds, digital assets, private capital, private debt, and other institutional alternative assets under management. Pension funds have become increasingly sophisticated in their investment strategies as well. During the last 10 years, more than 70 percent of the net increase in financial funds globally piled to those entities. And this trend is irreversible. Funds growth has been transitioning away from bank balance sheets due to two reasons: more attractive risk-return balanced propositions outside of the core banking sector and more tailored client service.

GPs are the companies that operate within this “off banking balance sheet” space and manage money for the insurers, sovereign and pension funds, for family offices of HNWIs, for banks investing into this space, and of course even for more demanding retail investors. Even Blackrock, the largest asset manager in the world, not only invests into funds operated by numerous GPs, but also owns some (like Global Infrastructure Partners), serves a lot of them as clients and is actively advocating the “integration of public and private markets” alongside the ability to scale private markets access for clients.

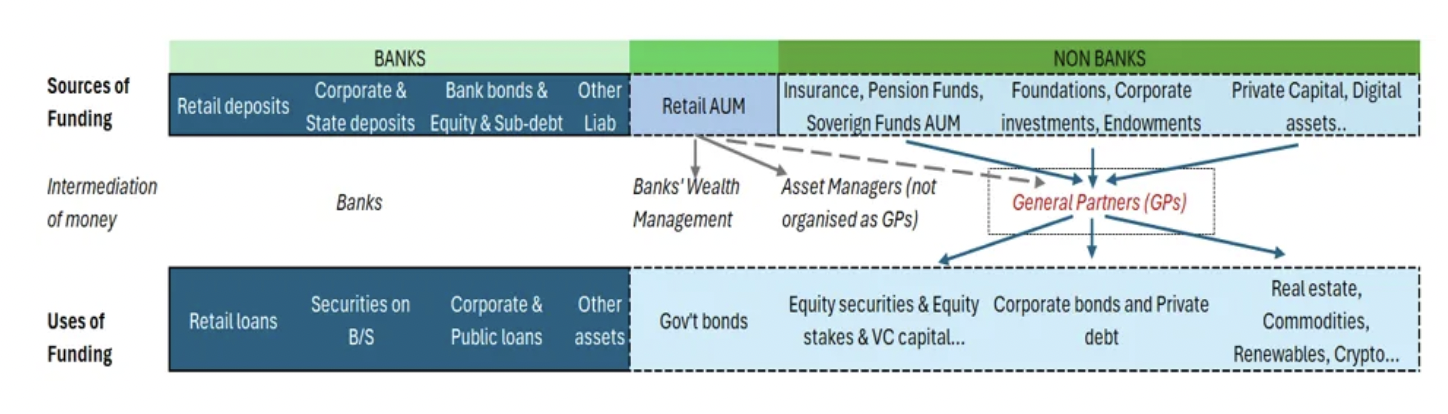

Graphically explained, GPs do business at this intersection of funds intermediation:

Note there is globally more than USD 200 trillion (!!) of sources of funds on the right side of the above graphic, with retail AUM being intermediated by both banks (those with asset management divisions) and non-banks.

To illustrate where this money is funneled to, see the last 15-year growth of two better known asset classes (Venture capital and Private Equity), which combined represent only a tiny fraction (ca USD 10 trillion) of where the above sources are invested into.

If you manage money for that tsunami of capital — you can sit in the best place in the entire investment chain. But that’s also super competitive market, and similarly to banking business, trust plays an absolute key role in this business. To earn it, you need to be consistently great in everything you do. Once consistently great, you can transform yourself into a money-making machine with limited downside and asymmetric upside business characteristics. Would you invest in such a business?

The Business Model of General Partners (“GPs”)

Why can this business be risk/return wise so attractive? Let’s dwell into a few core reasons, explained in a way for everyone to understand (as Tony Robbins does it in his book “The Holy Grail of Investing”[2]. How this business makes money and what drives its growth?

The Revenue Engine

As in every business, the company’s key attraction points are the revenue growth model and the scalability of profit margins. GPs manage alternative investment funds for qualified investors and earn their income from two primary sources:

- Highly predictable locked-in management fees: Typically, 2% of AUM (assets under management) per year and this mgt fee creates a constant cash flow payments to the GP from day 1. This is paid regardless of how successfully the GPs manage their investors’ money. There is no J curve effect with this business at all, once you kick-off the business of the ground, it starts making revenues.

- Performance related fee or Carried Interest: this is the GP’s share of the investment gains or profits they create for the investors and is usually 20% of the capital gain, while 80% goes to the investors.

Managing Money with Alignment

- GPs don’t just manage 3rd party money, they need to put their own cash in the funds they manage as a precondition, in other words they have to put their money where their mouth is. And industry standard dictates this need to be in the ballpark of 2% - 5% of the total funds under management. If they win, you win as the investor – if they lose, you lose. This approach becomes very cash-intensive for the GPs as they grow their business.

Crossing “the chasm”

Starting a GP business is brutally hard. The first fund requires trust you don’t yet have. First-time fund managers have an enormous confidence barrier to climb over.

My experience tells me that only after a GP reaches ~ EUR 1.0–1.2bn AUM does true scalability kick in. Managing at least 1 bn EUR (bare minimum) means that by that time you must manage several funds where your investors entrusted you with the money, and that you’ve returned them more than satisfying and benchmark-compared yields. In other words, you have market validated the consistency of your investment strategy and its meticulous disciplined execution. This sector is the pinnacle of finance business; it requires a lot of knowledge and execution power to be great. You fail once, you sub-deliver on the expected returns once -> you’re done, the trust is gone.

But if you deliver on your promise to your investors and you’ve crossed the chasm, the economics of GPs’ business model start to unwind in a pretty powerful way.

Example: with 1 bn EUR assets under management, GP locks-in 20 mil EUR management fees per year, which over the course of normal 5y investment period amounts to 100 mil EUR of revenue. Doing a solid job, this GP will return to investors at least 2,5x of the money managed (again over the course of 3-5 years post the investment period), making 20% of the 1,5bn EUR capital gain, which amounts to 300 mil EUR. That’s 400 mil EUR over the course of 10 years cycle per 1 bn EUR of funds managed. And that’s without the 2,5x multiple of their own money, i.e. 2% (or 20 mil EUR) the GP itself had to put into the business.

By reaching that level of AUM, the normalized profitability of a GP can range from 20%-50% of the topline, depending on the asset classes they manage. With nearly 100% dividend payout ratio. And it’s incredibly scalable, because with doubling of AUM, GP’s underlying costs (mostly experts work related) don’t come even close to doubling, just their investment bets become larger.

The GP business formula is effectively: recurring revenue + equity upside + forced liquidity recycling = compounding machine

Ultimate diversification creating asymmetric risk return investment

By owning a GP stake in i.e. multi-asset class GP, or owning several GP stakes across several asset classes, one can achieve ultimate diversification.

1. By the types of assets you own (equity, debt, real estate, renewables, venture capital, even fund of funds…)

2. By the unique industry skillset and experience (SW, healthcare, FMCG, financial services, technology…) of the funds in which you own a stake

3. By geographical focus

4. By the vintages of funds (past, present, and future) managed by the GP

5. By the portfolio of companies or assets within each fund managed by the GP

The probability that all asset classes will perform poorly in a correlated manner across such a diversified set of assets and across such different industries, geographies and different economic cycles is very low. But the upside can be high.

How To Invest into GP and Who is an Ideal Investor?

Why would the owners of GP sell a part of their business to outside investors in the first place? The answer lies in their own success. The more successful they are, the more money they attract to manage, and the more money they need to put into the business on their own. Given the constantly rolling cycle of exits (sales) from their fund portfolio companies, raising new funds for new acquisitions and paying out their LPs, those GPs which grow rapidly need a constant flow of their own cash to follow up.

Hence an acquisition of a GP stake is predominantly done via recapitalization of the firm, with the second most important factor to GPs willing to on-board a new co-owner of their firm being the expanded access to an LP base which such a new owner could bring. That basically tells you that a “perfect fit” investor into a GP stake is an experienced and well networked professional / institutional investor (insurer, a GP focused fund, a specialized bank or HNWI which operates in the asset management space).

Retail investors? Unfortunately, only after a potential listing of such GP at a later stage, as outlined below in the Final View chapter.

What to Expect from a Proprietary-Sourced GP Investment?

- Constant flow of dividends, ranging from high single % IRR digits to 15%/20% IRR per year as the GP scales, pretty much continuously, starting from year 1[3].

- Extremely well protected downside and a lot of upside subject to GP’s successful capital gain creation record (carried interest portion), fueling further growth.

- High probability of numerous exit options at attractive money multiple if you enter on normalized market comparative terms and decide to cash out at one point of time.

- Possibilities to co-invest alongside GP in any transaction within the wide portfolio of opportunities across investment classes at usually no-fee/no capital gain sharing mechanism.

- But what’s most important, and unlike with any other investment class, this outcome can be expected with rather high probability.

Final View: Where to Start Looking

The world’s best GPs, although corporately structured somewhat differently due to their massive scale (Blackstones, Appolos, KKRs of these world) are already publicly listed, and their valuations are high for a good reason. We are talking trailing P/E ratios of 25-65x (compare that to traditional banks with P/E of 6x-10x) and P/B over 3x (depending on the methodology used, as book values for asset managers might not reflect high intangible value of GP relationships, fee streams, carried interest etc) vs. bank’s average P/B of 1,0x. For an average retail investor, public markets are the only path to own a part of a GP, but given the entry price, the economics of such ownership are not quite like the ones I described above.

There are also specialized and fast-growing funds (the largest one being Blue Owl Capital with close to USD 300 bn AUM) which invest only in GP stakes, but again, doors to those are closed to retail investors.

Hence to seek for GP stakes opportunities across the USA/West Europe landscape, the search might be futile even for a well-suited investor.

However, quite overlooked, at the outskirts of Western Europe, lies South-East Europe, with some 15 years of catch-up to do behind the West in terms of AUM growth base, but with the highest % AUM growth rate of them all. Coupled with the smallest number of funds and GPs operating in the region on a comparative basis (see graphic below).

With only one (1!) single GP about to fulfil the outlined “getting across the chasm” EUR 1bn threshold during the next 2 years and multi-asset class investment strategy behind a strong execution capacity and professional investors’ relations.

If you’d like to explore this space — or you see the underlying logic and math as attractive — reach out. And welcome to one of my favorite worlds.

[1] Source: https://www.forbes.com/councils/forbesfinancecouncil/2022/11/18/gp-stakes-what-you-should-know-about-designer-financial-structures/

[2] Source: Tony Robbins, Christopher Zook: The Holy Grail of Investing; 2024

[3] Of course, depending on your entry ticket price